Free Report #18: UFP Industries (UFPI)

UFP Industries (UFPI)

I have begun to realize that the most recent issues I have written about recently tend to be large industrial manufacturing firms. Despite what you may think, this is not actually by design.

I think I have been gravitating to these companies lately for a couple reasons:

Easy to understand

Asset heavy

Inflation/Recession resistant

FCF generative

Now yes, I know, these are pretty “typical value investor” type of stocks. However, I have found that reviewing these types of companies a fresh of breath air, considering all the zaniness in the markets in 2021 (short squeezes, SPACs, Dogecoin, etc).

Normally, I would consider passing on most of these stocks, thinking that growth is simply not as strong as other more “modern” stocks. Here’s the hard truth I have learned: A well managed company, no matter the industry, has the potential to compound shareholder returns.

So, think of these newsletters as me giving these companies their fair shake of market analysis. They probably aren’t talked about much elsewhere, so I hope that these newsletters provide some value to you.

I don’t know how much longer this trend will continue, so stay tuned :) Do be sure to let me know if you like this type of analysis, or you would prefer me to do different stocks. I’m all ears!

With that out of the way, let’s dig into this week’s large industrial manufacturing company: Universal Forest Products Industries (UFPI).

Principle #1

A Business That We Can Understand

History

First, some brief history. UPFI has been around for a while, since 1955 to be exact. The with humble beginnings in Grand Rapids, Michigan, as a simple lumber production facility, but quickly grew in size and locations.

In 1979, the company made it’s first lumber delivery to a small, brand-new company, The Home Depot. From there on, the two companies have enjoyed superfluous growth off one another.

In 1993, UFPI went public on the Nasdaq. UFPI put that IPO money to good use. After five years and a few key acquisitions, the company became one of the largest lumber producers in the nation.

From then on, the company continued to make great strides in expanding the business on both in the industrial sector, but also on the consumer sector. They a specifically well-known creator of trusses for roofs.

Last note about the company: they have been profitable every year since inception. Talk about consistency!

Present Day

In 2021, UFPI operates on a global scale, with over 180 production facilities, 15,000 employees, and over $5B in revenues.

The company also serves four major customer bases:

Retail: Home Depot, Lowe’s, and independent buyers

Construction: Home and commercial builders

Industrial: Industrial packing and composite materials

International: Selling and sourcing their products overseas

The company currently has approximately 156 facilities and parcels of land located throughout the United States, Canada, Mexico, Europe, Asia, and Australia.

UFPI’s Retail division currently is the largest, representing over 36% of sales. These include brands that are either B2B or B2C. The retail division is strong and diverse. It ranges the gamut from selling lumber to build your deck, or just to build a simple birdhouse.

The Retail base has also grown rapidly, especially with the COVID-19 pandemic. Retail customers are putting more money improving their homes, since they have been spending more time in them.

Ditto for the homebuilding market (UFPI’s Construction segment).

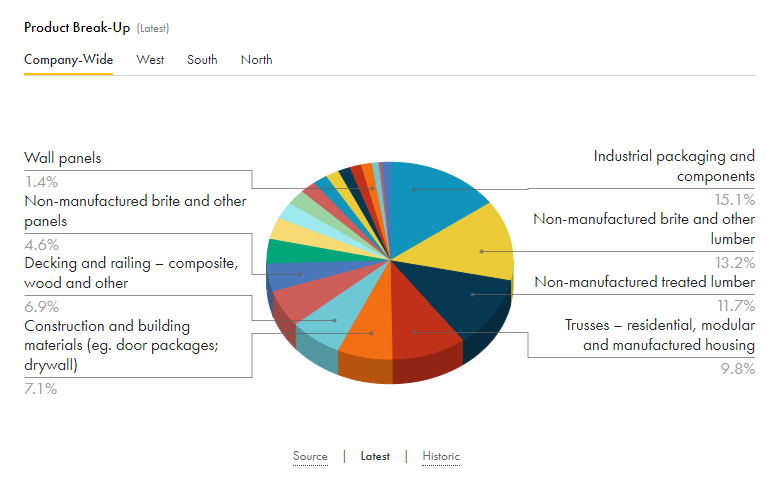

That being said, UFPI still boasts an impressive diversity in products. Check out the product break up below, courtesy of Tijori.

Verdict

UFPI is operating healthy and diverse business that appeals to both industrial and consumer markets. The customer bases are strong and ever-present. We will always be building things, and lumber is a literal building block of society.

Score: 1 Point

Principle #2

A Business That Has Favorable Long-Term Prospects

Growth Drivers

Again, if you have read my most recent issues, you will see a similar trend for these type of companies’ growth prospects: Mergers and Acquisitions (M&A). UFPI is no different here.

In fact, UFPI has been quite aggressive lately in M&As. Let’s dig a bit deeper.

M&A

Firstly, the company is pretty open and straightforward that their main quest for growth is M&As. They talk a lot of stereo-typical corporate speak here, but at least it is acknowledged by management to shareholders. They don’t seem to be peddling any unrealistic growth stories here.

As the CEO said above, the company has been on an acquisition spree lately. The company purchased five other businesses in 2020, and have completed six more in 2021 so far.

UFPI’s capital allocation strategy targets acquisitions to provide reasonable returns on investments. The company very nicely goes over each acquisition on their annual and quarterly reports, so I suggest you take a look if interested.

One specific acquisition I will mention is the purchase of PalletOne and Sunbelt Forest Products. This was one of UFPI’s largest M&A’s ever and the company has high aspirations for the two businesses. This is a big acquisition for the Industrial division, and will compliment UPFI’s consumer base considerably.

Organic Growth

Luckily, the company is not solely reliant on M&As to grow. In fact, UFPI has been doing an excellent job in innovating their product lines to improve efficiency and diversity.

UFPI defines new products as those that will generate sales of at least a $1 million per year within 4 years of launch, and continue to grow and penetrate the market. By creating waves of exciting new products, UFPI is allowing itself to grow new revenue streams.

This is especially important for the retail side of the company. For example, the new products like UFP-Edge shiplap and trim and ProWood Fire Retardant treated lumber contributed to 26% annual growth in new product sales.

Balance Sheet

Lastly, I just want to take a quick look at UFPI’s balance sheet. Management has been able to keep a very healthy balance sheet over the years, ensuring that assets cover liabilities almost two-fold.

This has allowed UFPI to take advantage of cheap debt, which they have taken advantage of for acquisitions.

Risks

Alas, not all businesses are perfect. UFPI most certainly has some risks we need to identify.

UFI is susceptible to the following risks, some of which are occurring right now:

General economic downturns

Fluctuating lumber costs

Availability of labor

Regulatory burdens

Lumber Price Swings

Let’s talk about the elephant in the room: lumber prices. Lumber is a commodity, and therefore is susceptible to wild market price swings. This famously occurred earlier this year, with lumber prices skyrocketing to all time highs in the spring.

Prices have since fallen back down to earth, to somewhat “normal” levels. These fluctuations both help and hurt UFPI.

While high prices support the selling of lumber in the Retail segment, it negatively affects the price of production in the Industrial and Construction segments. UFPI has no control over the costs and selling prices of lumber products, which are dependent on factors like government policies, environmental regulations, weather conditions, economic conditions and natural disasters.

These drastic swings in market prices will bring volatility to UPFI’s earnings and cash flow. UFPI cannot control this directly, but the focus of the company is to earn a stable average on profit per unit of lumber sold.

Dependence on Housing Market

UFPI is not only dependent on lumber prices, but the overall housing market with its Construction segment. UPFI has strong ties with homebuilders, and if demand for homebuilding decreases, then so will UFPI’s sales.

Lucky for UFPI, the housing market is in full swing across the nation. Everyone and their dog (especially dogs) want their own home. Homebuilding companies have their hands full at the moment, and UFPI is only happy to oblige.

Verdict

UFPI’s growth prospects seem pretty strong to me. I like the initiative they show by taking a sensible, yet forward-leaning approach to creating new products. M&A activity is strong, proving that UFPI is trying to become the consolidated industry leader.

My only concern is that UFPI makes sensible acquisitions, and not get too heavy handed by overpaying. But their balance sheet is strong for now, so that is a minor worry.

Score: 1 Point

Principle #3

A Business That is Operated by Honest and Competent People

CEO & Director

UFPI is led by Mr. Matthew J. Missad. Mr. Missad has quite the tenure with UFPI, first joining the company in high school as part of the maintenance crew! Throughout high school and college, he worked for the company, and UFPI even loaned him money to go to law school.

After graduating school, he was hired on with UFPI as the Director of Legal Compliance. From there, Mr. Missad has never left the company, and has had executive positions throughout his career, until being appointed as CEO in 2011.

This is definitely one of the coolest CEO stories I have heard in a while. If anyone knows UFPI inside and out, it’s this guy.

Small side note, the management team also has a long average tenure, with an average of over 15 years! Mr. Missad is only the 5th CEO to be appointed in the company’s 66 years of operation.

Very impressive!

Alignment

No surprise that UFPI is mostly institutionally held at this point in the company’s life cycle. It is nice to see that management owns over 2% of the company, which is a decent amount for the industry.

The largest individual owner is the CEO, Mr. Missad, who owns $22M worth of the company, which is over four times his annual salary.

ROIC and Profitability

I think it is safe to say that the CEO knows what he is doing. The amount of growth that UFPI has seen to its profitability since he took over is nothing short of astounding.

Gross margins are not super high, which is typical for the industry, but they are trending upward. Both ROIC numbers from Tikr and from the company are quite similar (included both for reference), which is great to see. Management seems to be hitting above their hurdle rate of 12% quite consistently.

Rewarding Shareholders and Capital Allocation

We already discussed that UFPI likes to conduct M&As and research new products with their cash. However, they also exhibit some pretty historically good shareholder rewards.

The company is committed to paying a dividend, which they have grown consistently every year by about 15%. The company is starting to conduct share repurchases, which I think are the right move for the company, and shareholders alike.

Verdict

I am really impressed by UFPI’s management team. The CEO and executive team is tenured, nearly all profitability metrics have grown, they have a growing and stable dividend, and debt and acquisitions are being managed properly.

Good all around!

Score: 1 Point

Principle #4

A Business That is Available at an Attractive Price

Free Cash Flow

This is actually the difficult part in my opinion. UFPI’s FCF has been lumpy throughout the last decade. This is simply due to the fact that UFPI is in the lumber business, and lumber remains a volatile commodity.

Looking at the chart below, it seems pretty messy, but there is both good news and bad news.

Good: The company has grown FCF by over 50% annually over the past decade (albeit erratically).

Bad: The P/FCF is also quite volatile, and sometimes expensive, making it difficult to find a normal level.

Nevertheless, I will strive to forecast this company’s FCF. I think that UFPI is likely to see strong growth, even with volatile lumber prices. I think the amount of M&As have been quite value adding, and think that these synergies will come to fruition soon.

I also have good trust in the experienced management that they will weather this temporary storm.

I will project FCF to continue growing FCF 15% from years 1-5, and then 8% 6-10. It will be very unlikely to actually follow this pattern, but I think the variable in growth rates will account for fluctuations in the lumber market.

Here comes the hard part: the terminal multiple. UFPI has fluctuated anywhere from 100x to -200x; lovely! That being said, UFPI’s profitability is strong and growing, and deserves a relatively high multiple. Therefore, I will assess a multiple of 30x.

Discounted Cash Flow

Here’s my DCF work on UFPI with zero margin of safety:

And here’s a 20% margin of safety:

Verdict

Current UFPI share price: $78.15

My buy price: $110.62

Another surprising DCF here. I was fully expecting UFPI to be fully valued. That being said, there is a good chance that these projections will be nothing close to reality, since lumber prices are so volatile.

Still, even if I lower the terminal value multiple to 20x, the company looks still look attractive. And that is with a 20% margin of safety!

I feel that UFPI is offering good value with a decent margin of safety. That is hard to find these days!

Score: 1 Point

Final Thoughts and Score

UFP Industries (UFPI) Score: 4/4

This was a very surprising report for me to write on. I had full expectations for a business of this quality to be at least fully valued, if not overvalued. I really was not expecting the company’s stock to be undervalued.

A pleasant surprise!

Before I make any investment decision on UFPI, I would need to research the company more in depth, as well as the lumber industry. The lumber prices have a huge affect on this company, so I would need to understand that aspect very well.

Overall, I really like this company and the management team. I think you could do a lot worse as an investor than choose this company.

Recommended Articles

CVS Deep Dive: Enlightened Capital

I just recently discovered Enlightened Capital’s Substack. He doesn’t have a lot of write-ups, but those he does have are of high quality, plus they are free!

His take on CVS is quite intriguing, and I will have to dig deeper for myself.

Music

This week’s music recommendation is quite different from my normal genre of music, which is usually metalcore. Yes, I actually do listen to other music from time to time…

I somehow missed Woodkid’s most recent album release last year. Must have been pre-occupied by a pandemic or something. Anyway, his 2020 album S16 is a true work of art. Woodkid’s use of percussion and orchestra never ceases to amaze me. The musical creativity here is staggering.

I also love Yoann Lemoine, (aka Woodkid’s) voice. When I hear it, I can’t help but think that this guy should be the next musician for the title track of a James Bond film.

Anyway, “Goliath” is the first track of S16, and you will immediately see what I mean by creative percussion. Some other standout tracks are “Reactor”, “Highway 27”, and “Minus Sixty One”.

Thanks for reading!

-Dillon Jacobs

Holdings Disclosure

Neither I nor anyone else associated with this website and newsletter has a position in UFPI and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of Stock Spotlight are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This report is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this report reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of Stock Spotlight) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature, and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

The views about companies and their securities expressed in this report reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA on whether to buy, sell or hold shares of any particular stock.

We did not receive compensation from any companies whose stock is mentioned in this report.

No part of the analyst's compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this report.