Free Report #22: Fiserv Inc. (FISV)

Fiserv (FISV)

I love reading quarterly hedge fund letters. As we are about to roll into the final quarter of the year, I eagerly anticipate to see what institutional investors have done during Q3.

I enjoy reading the letters not because I want to carbon copy what the super-investors are doing, but I am always curious to as to their insights, and whether or not they align with mine.

It forces me to review my own convictions, whether popular or unpopular, which I think is very important.

In fact, I compile a list of hundreds of these letters from the far corners of the internet each quarter and post them on my main site.

You can view the entire archive here if you want.

Anyway, I also visit Dataroma (great resource!) from time to time to see what the hedge fund managers are buying. Of course, there are some very obvious and well covered stocks like BABA, FB, and AMZN, that have been scooped up this year.

But I noticed one particular company that has seen a lot of buys this year on the street that I had never heard of: Fiserv Inc. (FISV).

This sparked my curiosity. Since I know next to nothing about Fiserv, I thought this week would be the perfect opportunity to explore the company.

Let’s dive into Fiserv.

Principle #1

A Business That We Can Understand

Overview

Founded in 1984, Fiserv provides financial services technology solutions to over 10,000 clients worldwide in the banking, insurance, healthcare and investment industries.

Fiserv customer base covers the entire gamut of the financial institutions, like banks, credit unions, leasing and finance companies, investment management firms, and billers.

The company has grown its business through developing highly specialized products and services and enhancing them, increasing capabilities through innovation, expanding client base, and acquiring complementary businesses.

Speaking of acquisitions, Fiserv recently merged with First Data in 2019. This allowed Fiserv to provide payment processing services for merchants. We will dive a bit more into this merger later on.

Business Segments

The company has three reportable segments:

Payments and Industry Products

Financial Institution Services

Merchant Acceptance/First Data

Let’s break down these segments.

Payments and Industry Products: This division is the largest organic one, and provides a myriad of services, such as:

electronic bill payment and

person-to-person payment services

account-to-account transfers

debit and credit card processing and services

Internet and mobile banking software and services

and many more

Financial Institution Services: This is the smallest organic segment that provides all things that are deal with account processing, such as things like:

item processing and source capture

cash management and consulting services

loan origination and servicing products

ACH and treasury management

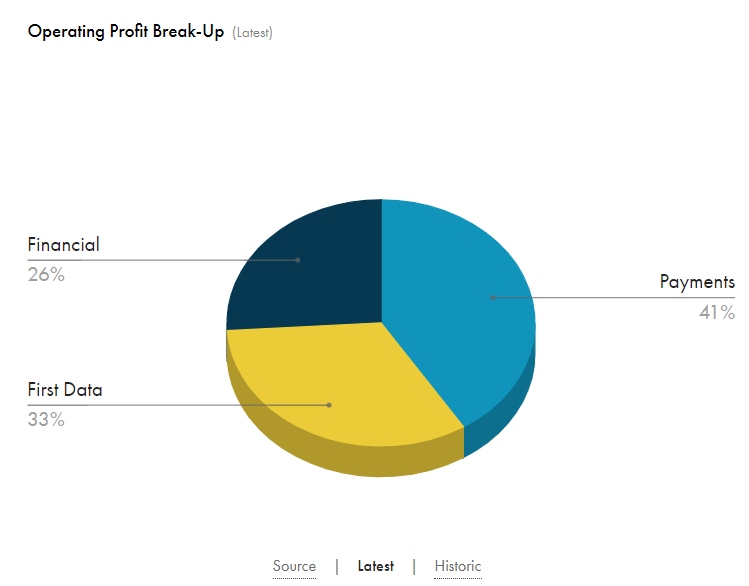

Merchant Acceptance/First Data: This is the largest segment that was acquired with First Data.

Merchant Acceptance mainly represents the commerce side of the company, which enables small and large business conduct every day by securing and processing of payments. First Data’s POS network, known as Clover, is large and has over 3,000 payments per second.

Even though Merchant Acceptance is a new division of the company, they represent quite a large portion of the entire revenue mix.

That being said, the Payments division is the most profitable of all, making up 41% of all operating profits. Merchant Acceptance comes in second with 33%, with Financial bringing up the remainder of 26%.

Verdict

Now, I will be the first to admit that Fiserv’s business sounds a bit airy, with a lot of “solutions” and “services” being provided that seem to never clearly be defined.

It’s definitely a harder company to understand than last week’s company, Gentex.

It may be hard for the average investor to understand exactly what these services are, but essentially, Fiserv is a Fintech company that handles all kinds of payment processing. They compete with (but also work with) the likes of others payment processors like Visa, Mastercard, Square, and Shopify.

This barely passes the “understandable” part of my analysis, but it only takes a quick read of a few pages in the annual report to gain a full understanding of the business itself.

If you aren’t willing to go the extra mile to understand the business, then this is probably not the company for you to invest in. But for me, it only took about 5 minutes of extra reading.

Score: 1 Point

Principle #2

A Business That Has Favorable Long-Term Prospects

As a Fintech company, Fiserv enjoys the large tailwind of increasing global digital payment adoption. However, Fiserv focuses on five key areas to improve their business:

I love seeing Capital Discipline here as one of their main pillars of success. This is a sign of good management, and ensuring that they stay committed to good deployments of capital.

Let’s identify some of the key growth drivers that I see for the company.

Growth Drivers

Acquisitions

Strategic and sensible acquisitions will be the primary growth driver for Fiserv. This is evident with their largest ever purchase of First Data.

However, in 2020, Fiserv managed to complete three smaller acquisitions:

MerchantPro Express

Bypass Mobile

Inlet

While MerchantPro expands the company’s merchant services business, Bypass enhances its omnicommerce capabilities and Inlet boosts its digital bill payment strategy.

So far in 2021, Fiserv recently bought its key distribution partner and technology company, Pineapple Payments, as well as Ondot Systems.

With Pineapple Payments, Fiserv will be in a position to expand the reach of its payments solutions, especially Clover and Clover Connect, which were acquired through First Data.

Ondot Systems is a digital experience platform for financial institutions. This acquisition enhances Fiserv's digital capabilities and strengthens its competitive position.

Growing and Diverse Product Portfolio

All of these acquisitions are being made in key areas in order to enhance the diversity of the company, specifically through mobile and e-commerce. Moreover, Fiserv is seeing growth where it needs to: in user base and transactions.

These bolt on acquisitions allow Fiserv to yield a steady flow of new customers, and is witnessing solid growth in account-to-account transfers and P2P.

On the mobile front, adoption has increased 15% quarter over quarter. Zelle transactions more than doubled in the reported quarter and improved 18% sequentially.

Additionally Zelle’s user base has almost tripled year over year. Backed by such strong demand, the company expects to witness more client additions moving ahead.

This growing number of transactions and users allows the network effect to compound for Fiserv. The larger the network grows, the more valuable it becomes.

Risks

Competition

As mentioned in the previous section, Fiserv’s core banking products and services are part of a highly competitive market.

The Fintech industry highly competitive with the entry of several non-banking bodies that offer both customer facing and back office financial technology products and services.

In the future, competition will most definitely increase as market entrants grow in number. The existing competitors will increase product lines and services with updated technologies to attract customers and retain the existing ones.

The industry growth will challenge Fiserv to maintain strong and long-term client relationships.

Integration

As a serial acquirer, Fiserv has some serious integration risk. M&A’s may not always work out as planned or take longer than expected, which comes at the expense of shareholders.

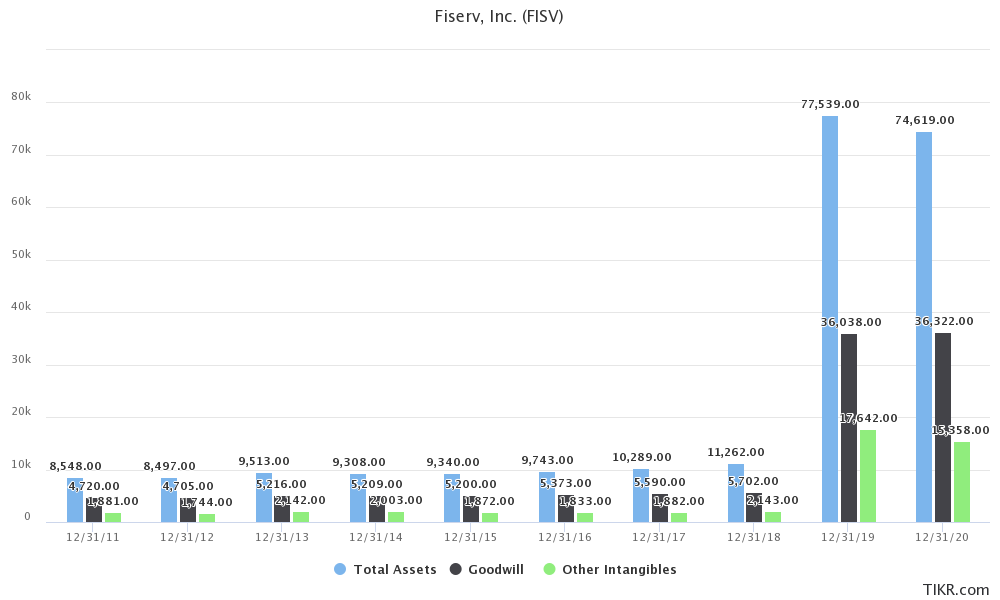

Acquisitions also have a tendency to negatively impact the balance sheet in the form of a high level of goodwill and intangible assets.

In Fiserv’s case, goodwill and intangibles consist well over half of the total assets on the balance sheet. Frequent acquisitions are a distraction for management, which could impact organic growth.

Debt

Fiserv’s total cash is around $900M, which is plenty to take care of their short-term debt.

However, the cash position pales in comparison to their long-term debt balance of over $20B!

With all the acquisition activity, Fiserv’s management will have to be absolutely positive that their cash flows can grow enough in order to pay off this debt eventually. If not, then the company will be in some serious trouble.

Verdict

I love the Fiserv’s business model, but I am not a big fan of they way they are growing. Serial acquirers historically do not turn out well for shareholders.

I am also not a big fan of the balance sheet and the debt situation. I would prefer to see a lot more tangible assets, especially cash. Debt could turn out to be a big issue if not handled correctly.

Also, this does not even take into the account of a seamless transition of the acquisitions.

I am seeing too many risks here for me to feel comfortable with the growth model.

Score: 0 Points

Principle #3

A Business That is Operated by Honest and Competent People

President & CEO

Mr. Frank Bisignano currently serves as the President and CEO of Fiserv. Mr. Bisignano was just recently appointed as CEO in 2020. Before becoming CEO, Mr. Bisignano was the Chairman and CEO of First Data, so he seems a natural fit as the company’s leader.

During his time as CEO, Mr. Bisignano led First Data to its $2.6 billion initial public offering in 2015, the largest U.S. IPO of the year. Before First Data, Mr. Bisignano served in over 30 years in executive leadership roles in finance institutions, such as JP Morgan Chase and Citigroup.

Mr. Bisignano succeeded previous Fiserv CEO, Jeffery Yabuki.

| Twitter")

Mr. Yabuki was a very well known and respected CEO in the company and industry. He stayed on until 2020 to see most of the First Data acquisition through, and then retired to focus on other philanthropic endeavours.

Mr. Yabuki's 15 year tenure as CEO resulted in massive growth for the company, achieving a whopping 969% shareholder return rate.His leadership resulted in Fiserv being named to Fortune's most admired companies for a seven year streak.

Mr. Yabuki is going to be an extremely tough act to follow, so Mr. Bisignano certainly has his work cut out for him. The company currently has decent reviews on Glassdoor, with Mr. Bisignano achieving a 65% approval rating.

Alignment

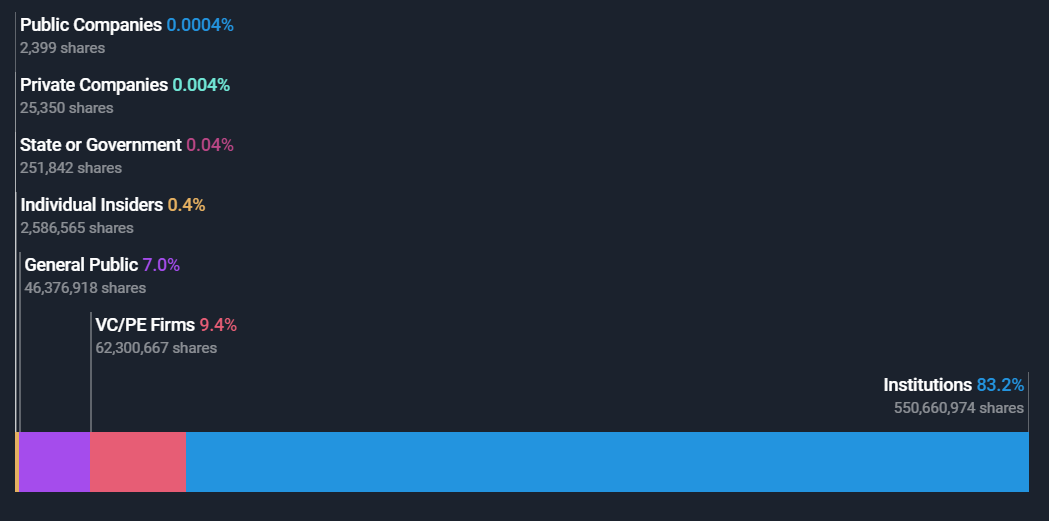

As a large $72B company, Fiserv is mostly institutionally held. Relative to his net worth, The CEO actually owns a decent portion of the company, at over $200M. This is 24x his annual salary, so this is nice to see.

Outside of institutions, Fiserv is over 9% owned by the private equity firm, KKR & Co. There a plethora of other funds and investors with significant stakes in the company, such as Longview Partners and ValueAct Capital.

ROIC and Profitability

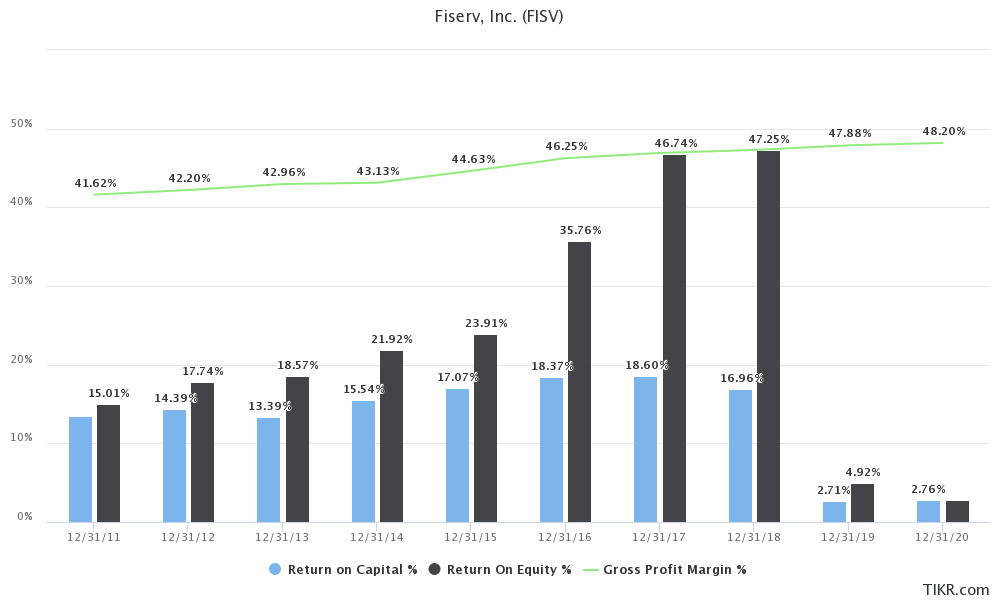

At first glance, it may look like Fiserv’s quality took a massive dip, since ROE and ROIC were at all time highs until 2019. This was obviously due to the massive restructuring the company undertook for the First Data acquisition.

This is simply due to the fact that the company is still working through the restructuring and has yet to fully integrate. This should level out within the year. One good thing to see is gross margins have slowly increased over time, which is excellent to see.

Fiserv’s track record is solid.

Rewarding Shareholders and Capital Allocation

Fiserv is all about rewarding shareholders through acquisitions. In order to fund these acquisitions, Fiserv has been diluting shareholders, which is not very pleasant. Shares are higher now than they were 10 years ago.

Before the issuance, Fiserv was buying back shares consistently. It would be nice to see this continue into the future in order to boost total shareholder return.

Fiserv does not pay a dividend.

Verdict

While I am not seeing any major red flags here, there are more things I dislike than I do like.

Mr. Bisignano seems to be a good leader, but is brand new in the position, and has to follow up Mr. Yabuki, who I would have prefered to have as a CEO.

If Mr. Yabuki was still on board, I would feel much more at ease.

I also am not a fan of the dilution, for shareholders as I prefer companies to bankroll the acquisitions through their own operations, or with smart debt.

Score: 0 Points

Principle #4

A Business That is Available at an Attractive Price

Free Cash Flow

As you can see below, FISV has had some pretty steady growth and multiples, until the First Data acquisition in 2019. Due to the massive increase in cash flows post acquisition, FISV’s P/FCF have returned to a normal level of around 22x.

The First Data acquisition seems to have increased FCF dramatically, which is great to see.

I find it quite difficult to project FCF due to all the recent M&A activity and integrating that is still needed to be done. Prior to First Data, FISV was compounding FCF around 7% per year. Post First Data, the company has compounded at a 26% rate, but for only two years.

To keep estimates conservative, I will assess that FISV will grow FCF at a pre First Data growth rate of 7% as it completes all major integrations, and then proceed to ramp growth up to 12% when all acquisitions are completed and integrated.

P/FCF will be at around a 20x multiple.

Discounted Cash Flow

Here’s my DCF work on FISV with zero margin of safety:

And here’s a 20% margin of safety:

Verdict

Current FISV share price: $109.74

My buy price: $76.14

FISV seems to be fully valued, if not overvalued right now. The market seems to have already priced in the seamless integration of the acquisitions and growth of cash flows.

Just for fun, I went ahead and put in the shares outstanding that were on record pre-First Data to see what the value per share would be. Lo and behold, it’s above the current share price.

This is why I don’t like dilution.

Score: 0 Points

Final Thoughts and Score

Fiserv (FISV) Score: 1/4

In this shallow dive on Fiserv, I found too many risks that seem to outweigh the rewards. Looking back, nearly everything looks great.

Here’s what I like:

Explosion of FCF growth

Solid core business

Great historic management

Looking forward however, presents a different story:

New CEO risk

Integration risk

Debt risk

Share dilution

Overvalued stock price

For me, this is just too much risk. But this is only on a shallow dive of the company. There could be many things I have overlooked or missed about Fiserv that could be crucial in my analysis.

And this may be very possible. I was first intrigued at the amount of hedge funds buying this company, and they assuredly know more about Fiserv than me.

But that’s OK. We all have different risk tolerances. What may seem like a good deal for some of these hedge funds will inherently be too much for me.

Recommended Reading

I thoroughly enjoyed this analysis on TTWO from Punch Card Investor. I am tremendously bullish on video games in the future, and I think that TTWO offers some great value in this regard.

I also wrote on TTWO a few months ago, and gave them a perfect 4/4 score.

Music

Sleep Token’s new album, This Place Will Become Your Tomb, was finally released last Friday. I highly encourage you to give it a listen, as there is just so much to unpack here.

I picked my favorite track “Telomeres” to highlight this week, but honestly, there are many that competed for this spot. Ironically, the song sounds least Sleep Token-like, and I hear a lot of Deftones influences here.

Upon the first couple listens, I don’t know if I enjoy it more than their debut album Sundowning, but I am positive it will grow on me the more I listen.

Some of the other standout tracks here for me are “Hypnosis”, “Like That”, and “Atlantic”.

It Takes Two Seconds to Share This Post

Chances are that if you have read this far, then you probably know someone else who could benefit from my insights. Before you close out, maybe you could take a moment and share it with a friend? Doing so really helps the growth of this weekly newsletter.

Thanks!

Holdings Disclosure

Neither I nor anyone else associated with this website and newsletter has a position in FISV and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of Stock Spotlight are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This report is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this report reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of Stock Spotlight) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature, and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

The views about companies and their securities expressed in this report reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA on whether to buy, sell or hold shares of any particular stock.

We did not receive compensation from any companies whose stock is mentioned in this report.

No part of the analyst's compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this report.